BJCC Golf and Country Club News

BJCC Golf and Country Club News

If you love golf you're going to love this! What puts a smile on your face? Golf?

I am making a plea to all members to refrain from making any personal attacks, threatening or otherwise to people in our state government or to members of our club.

Best Regards,

2. There has been requests that the LC have a session to meet and

inform members on the outcome of the meeting and actions initiated by

the LC to date. And we are happy to inform you that we have arranged to

hold this session on Friday, 20 Jan 2012 at 8pm at the coffee terrace.

The sequence of play is: Holes # 10, 11, 12, 13 then followed by Holes # 5, 6, 7, 8 and 9. In other words, Holes # 14, 15, 16, 17 & 18 be replaced by Holes # 5, 6, 7, 8 & 9 .

LIAISON COUNCIL FOR THE YEAR 2012

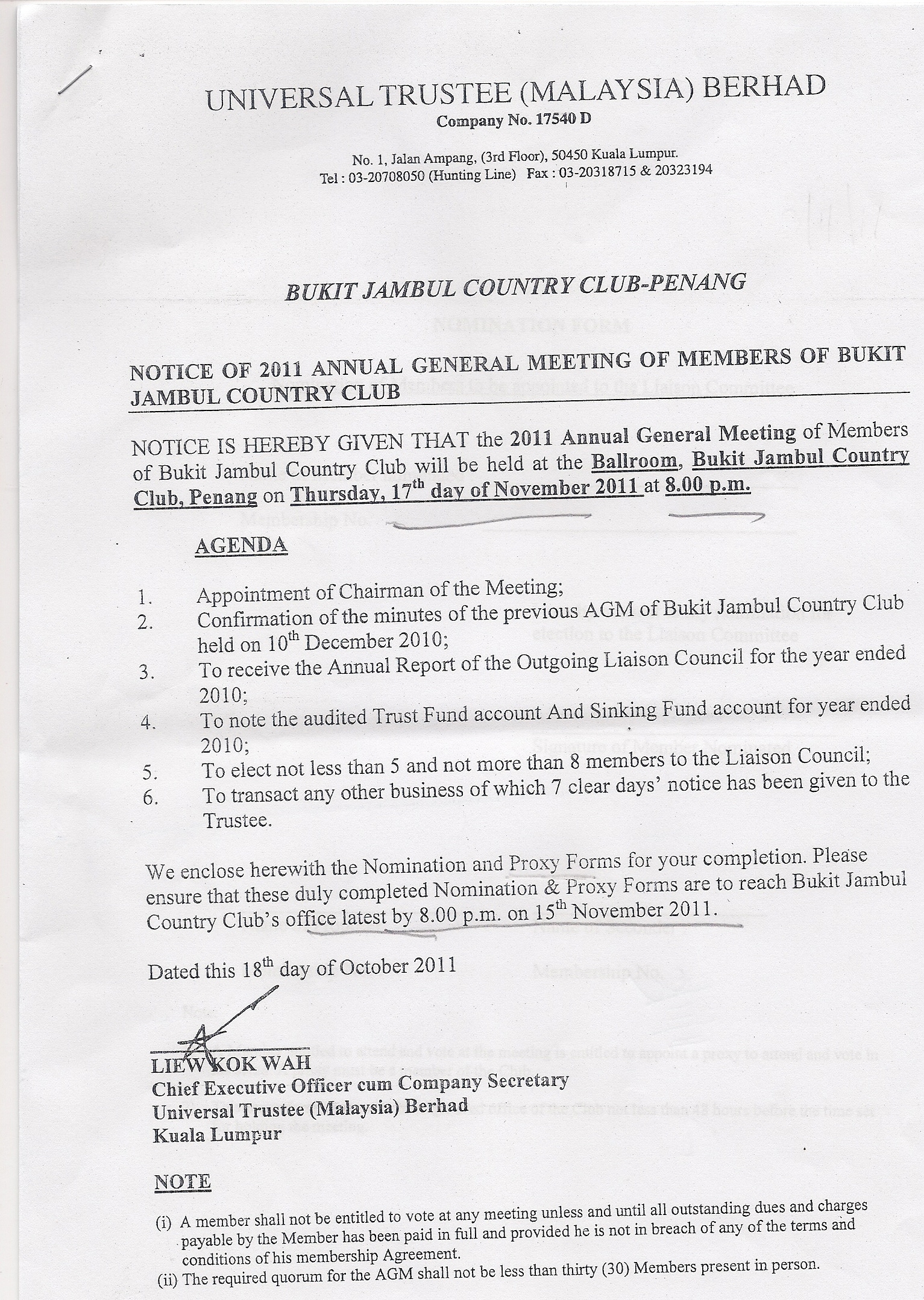

AGM 2011

BJCC management fiasco: 'Outsourcing not the fair way ...

Golfers pleads Guan Eng to intervene

Bukit Jambul Country Club fiasco

Golfers Protest over new Buggy Rule

http://komunitikini.com/

http://www.guangming.com.my/

http://www.guangming.com.my/

(one can translate that to English....click some keys)

Thugs & Secuirty Guards used to guard BJCC's fairway

The Star Feb 1 & 3:

Club managing director Datuk Eiro Sakamoto said the upgrade includes the purchase of additional 60 electric buggies for hire at a fee to "make more money"!

Golfers speak out against buggy ruling

Dutuk Dr Chatar Singh 82, a member since 1984, said the ruling was not suitable due to the club's structure. "The design was meant to enable golfers to walk around the course as the parking lot (for the buggy) is a distance away".

Member Tony Lim said the management also increased the buggy rental rates from RM22 to RM37 for the first nine holes. He added that using a buggy to play golf was pointless because the golfers enjoyed walking.

Bayan Baru Barisan co-ordinator Por Joo Tee said that decision made should be a balance between profitability and corporate social responsibility. "I will write to Penang Chief Minister Lim Guan Eng, who is also Penang Development Corporation (PDC) chaiman, to look into the matter," he said when met at the club's on Wednesday.

Japanese firm Taiyo Resort (KL) Bhd took over the club's management in 2010 and signed a leasing agreement with PDC and Island Golf Properties Bhd.

Shttp://www.theedgeproperty.co

However, even at St Andrews members can still walk!

Member Tony Lim said the management also increased the buggy rental rates from RM22 to RM37 for the first nine holes. He added that using a buggy to play golf was pointless because the golfers enjoyed walking.

Bayan Baru Barisan co-ordinator Por Joo Tee said that decision made should be a balance between profitability and corporate social responsibility. "I will write to Penang Chief Minister Lim Guan Eng, who is also Penang Development Corporation (PDC) chaiman, to look into the matter," he said when met at the club's on Wednesday.

Japanese firm Taiyo Resort (KL) Bhd took over the club's management in 2010 and signed a leasing agreement with PDC and Island Golf Properties Bhd.

Shttp://www.theedgeproperty.co

However, even at St Andrews members can still walk!

USGA Declares War on Riding!

A serious campaign to

increase the number of golfers who walk is now underway by the United

States Golf Association. The Golf Journal, official publication of the

sport’s ruling body, launched a dramatic appeal headlined “Declare

Yourself a Walker.”

Taking aim squarely against “the myths of golf cars,” David Fay, USGA’s Executive Director boldly states “We strongly believe that walking is the most enjoyable way to play golf and that the use of carts is detrimental to the game. This negative trend needs to be stopped now before it becomes accepted that riding in a cart is the way to play golf.”

The pronouncement is strong and specific, castigating those courses that have jumped on the riding bandwagon. While pointing out that the majority of U.S. courses have no policy requiring mandatory use of carts, USGA targets the more than 1000 places that do.

Returning golf back to its original nature is the century old organization’s justification for its new campaign. Putting its money where its mouth is, USGA is publishing its “Call to Arms” –an informative booklet, distributed free to the public. Titled A Call to Feet: Golf is a Walking Game, the detailed free booklet is available simply by calling USGA headquarters in Far Hills, N.J. at (908) 234-2300.

For years, individuals have been invited to become USGA members. Now, such golfers are asked to make a more serious commitment. The announcement requests that members sign and mail in the USGA Walking Member Declaration. Its text reads:

“. . .By signing this, I hereby give my oath that I will never ride in a golf cart for a round of golf unless it is forced upon me or I develop a physical condition which necessitates the use of a cart. Whenever given a choice, I will always walk.”

Members then receive a bright yellow bag tag, emblazoned with USGA’s logo, identifying the person as a Walking Member and bearing the full text of the Declaration oath.

By tradition, the USGA’s leadership has stood above commercial interests, resisting pressures to pervert the spirit and heritage of the sport. Doubtless there are people who, despite logic and evidence to the contrary, still will argue that riding is inherently faster than walking–or that rental revenue is essential to golf clubs and courses. Numerous examples kibosh these assertions, according to the USGA which has conducted many studies and thorough investigations.

For example, Pinehurst Resort and Country Club is cited, where walking and carrying your own bag is optional now on four of the property’s seven courses–1,3,4, and 5. (Walking’s still allowed on the famed Number 2 course but only with a caddie.) “It’s not slowing down play at all, and the courses are still packed. Granted, the policy hasn’t been in effect all that long, but I haven’t heard one negative comment yet.”

This trend toward providing players the opportunity to walk is expected to accelerate, as a result of USGA’s walking campaign. We encourage advocates of walking golf to pledge your oath and promote the USGA’s Walking Members Declaration!

Taking aim squarely against “the myths of golf cars,” David Fay, USGA’s Executive Director boldly states “We strongly believe that walking is the most enjoyable way to play golf and that the use of carts is detrimental to the game. This negative trend needs to be stopped now before it becomes accepted that riding in a cart is the way to play golf.”

The pronouncement is strong and specific, castigating those courses that have jumped on the riding bandwagon. While pointing out that the majority of U.S. courses have no policy requiring mandatory use of carts, USGA targets the more than 1000 places that do.

Returning golf back to its original nature is the century old organization’s justification for its new campaign. Putting its money where its mouth is, USGA is publishing its “Call to Arms” –an informative booklet, distributed free to the public. Titled A Call to Feet: Golf is a Walking Game, the detailed free booklet is available simply by calling USGA headquarters in Far Hills, N.J. at (908) 234-2300.

For years, individuals have been invited to become USGA members. Now, such golfers are asked to make a more serious commitment. The announcement requests that members sign and mail in the USGA Walking Member Declaration. Its text reads:

“. . .By signing this, I hereby give my oath that I will never ride in a golf cart for a round of golf unless it is forced upon me or I develop a physical condition which necessitates the use of a cart. Whenever given a choice, I will always walk.”

Members then receive a bright yellow bag tag, emblazoned with USGA’s logo, identifying the person as a Walking Member and bearing the full text of the Declaration oath.

By tradition, the USGA’s leadership has stood above commercial interests, resisting pressures to pervert the spirit and heritage of the sport. Doubtless there are people who, despite logic and evidence to the contrary, still will argue that riding is inherently faster than walking–or that rental revenue is essential to golf clubs and courses. Numerous examples kibosh these assertions, according to the USGA which has conducted many studies and thorough investigations.

For example, Pinehurst Resort and Country Club is cited, where walking and carrying your own bag is optional now on four of the property’s seven courses–1,3,4, and 5. (Walking’s still allowed on the famed Number 2 course but only with a caddie.) “It’s not slowing down play at all, and the courses are still packed. Granted, the policy hasn’t been in effect all that long, but I haven’t heard one negative comment yet.”

This trend toward providing players the opportunity to walk is expected to accelerate, as a result of USGA’s walking campaign. We encourage advocates of walking golf to pledge your oath and promote the USGA’s Walking Members Declaration!

RESPONSES by LC & UT

Dear BJCC Members:

It has been brought to our attention that several unwarranted, foul-language statements/words had been sent out to people outside our members. Such are unacceptable and unwelcomed. We won't tolerate any of these.

Members understand that the platform be used to share our views and opinions. I have kept reminding everyone that we are members of a reputable club and all of us needs to try and maintain certain decorum when we wish to express certain disagreements and dissatisfaction. It is impossible to have a state where views and interpretations won't differ.

I am making a plea to all members to refrain from making any personal attacks, threatening or otherwise to people in our state government or to members of our club.

Thank you for your support and co-operation

Best Regards,

Stanley Park Feb 6, 2012

1. Liaison Council (LC) will be meeting with Dato Sakamoto on Thursday, 19 Jan 2012. We have on our agenda for discussion pertinent issues affecting members of BJCC.

2. There has been requests that the LC have a session to meet and

inform members on the outcome of the meeting and actions initiated by

the LC to date. And we are happy to inform you that we have arranged to

hold this session on Friday, 20 Jan 2012 at 8pm at the coffee terrace.

Letters to BJ UT 0112

NOTICES

(1) Revised Sequence of Play

The management has informed that members will be playing a new sequence of 9 holes golf, a combination of 4 old and 5 new holes effective from Saturday, January 1, 2012.The sequence of play is: Holes # 10, 11, 12, 13 then followed by Holes # 5, 6, 7, 8 and 9. In other words, Holes # 14, 15, 16, 17 & 18 be replaced by Holes # 5, 6, 7, 8 & 9 .

- Players must play the 9 holes in sequence, no skipping of hole is allowed.

- Tee-off time is 7.00am. Teeing off before 7.00am is strictly not allowed. Players must start from the 10th tee. They shall not commence play from any other holes.

- Buggies are allowed to go onto fairways unless management announced otherwise.

The above course control is being implemented during this interim period until the renovation of all the 1st Nine Hole is ready for play.

Disciplinary action will be taken against any players who infringe any of the local rules and regulations above.

(2) With effect from February 1, 2012, the 1st Nine Holes will be opened for play

Disciplinary action will be taken against any players who infringe any of the local rules and regulations above.

(2) With effect from February 1, 2012, the 1st Nine Holes will be opened for play

- Golf Registration counter will open at 7:00am daily.

- Tee off time is 7:30am daily. Players must commence play from 1st Tee and not from any other holes.

- Buggy is compulsory for all players, not for free but at a fee ranging from RM37.10 to RM95.40 with 6% Govt Tax, depending players are members, guests/visitors, playing 9 holes or 18 holes.

- Caddy Fee - Monday~Friday: RM35.00 + 6% Govt. Tax (RM47.70); Sat, Sun. & Public Holidays: RM50.

- Walking Golfers are allowed to play from Monday to Thursday. The tee off time is 5:00pm. Players are required to register themselves personally and to collect their starter chits. Booking can be made from 4:30pm onwards on these days (Monday to Thursday except on Public Holidays)

(3) To cut cost effective from Monday, January 9, 2012, service at golfers' changing rooms (shower toilet) shall be closed at 8:30pm daily instead of 10:00pm normally due to few golfers using them

Members and guests who want to use shower and toilet facilities may go the swimming pool complex.

Notes: Interesting news:

Members and guests who want to use shower and toilet facilities may go the swimming pool complex.

Notes: Interesting news:

AGM 2011

Tom Krazit writes about the ever-expanding world of Internet search, including Google, Yahoo, and portals, as well as the evolution of mobile computing. He has written about traditional PC companies, chip manufacturers, and mobile computers, spending the last three years covering Apple.

Tom Krazit writes about the ever-expanding world of Internet search, including Google, Yahoo, and portals, as well as the evolution of mobile computing. He has written about traditional PC companies, chip manufacturers, and mobile computers, spending the last three years covering Apple.

{kind=link}